Blockchain Explained – Why The Hype?

Chances are that you’ve been hearing all about Bitcoin and cryptocurrencies lately. In 2017 alone the value of Bitcoin increased more than fifteen times. But as great as Bitcoin and other cryptocurrencies are it’s the underlying technology that is really exciting. Looking to have blockchain explained in a simple way? Then you’ve come to the right place!

Blockchain network technology helps to create the economic ecosystems in which cryptocurrencies like Bitcoin operate. So, what is blockchain network technology, how do these networks support cryptocurrencies, and what makes this technology so special?

To put it simply a blockchain network is a shared database that eliminates the need for third party intermediaries. This is important because it enables a decentralized exchange of trusted data. Blockchain technology uses cryptography to ensure data is secure and uses consensus algorithms to guarantee the integrity of information.

What Are Centralized Ledgers?

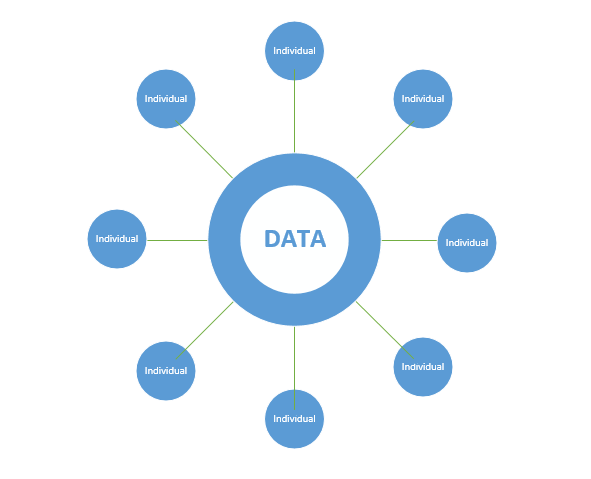

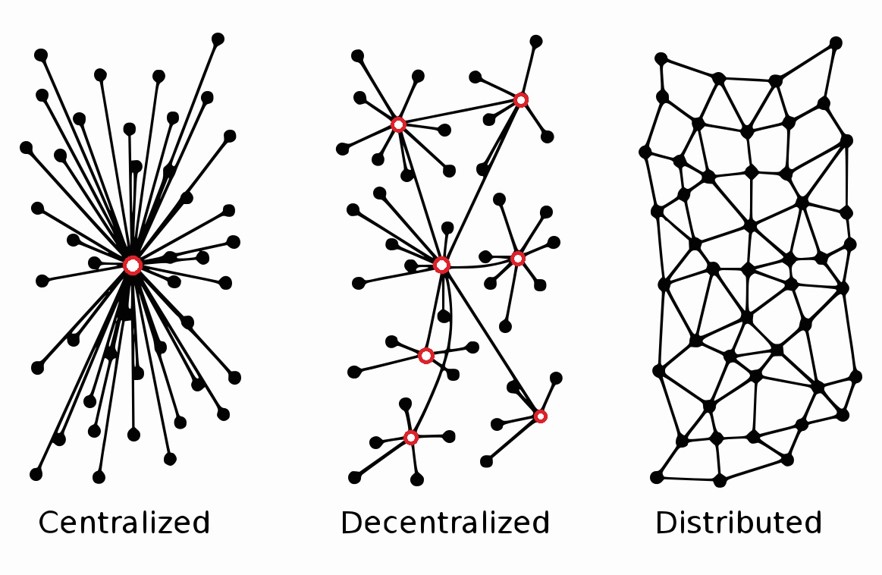

Let’s first try to understand how a decentralized ledger is different from a centralized ledger. Think of the bank that you hold an account with. You and all the other account holders of this bank are trusting the institution to store and keep track of all relevant data. This can be the amount of money in your account or the transactional data that is generated every time you swipe your debit card.

All account holders are feeding information to one central database. They trust that the manager of this database can keep this information organized and secure.

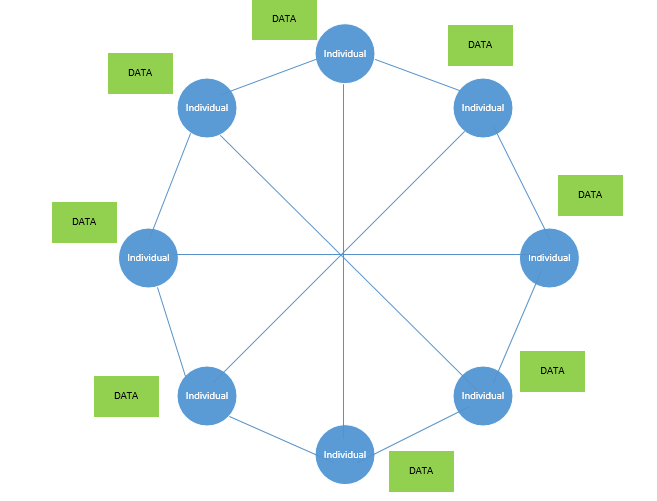

But what if all the account holders shared in the management of this database? What if they did not solely rely on the institution to maintain data integrity? What if every person who held an account at the bank could have access to a ledger that contained not only their own information but the information of everyone else?

The whitepaper written by Satoshi Nakamoto detailing the functionality of the Bitcoin blockchain explained how this could be done. The ledger containing important information does not have to be centralized any longer. All network participants can be responsible for maintaining their individual ledger of accounts.

How Does A Decentralized Ledger Work?

So, how does this work in practice?

Let’s say I want to pay you five dollars for reading this article . We are both participants of the same blockchain network. There are also other individuals that use the network simultaneously. I send the money to you and once the transaction is approved all the ledgers in the network update.

But let’s say there was a mistake and my ledger did not update correctly. We can easily figure out which ledger is incorrect by comparing all the ledgers in the network to each other. If my ledger is different than all the others we can quickly determine that it contains an error.

Trust and data accuracy no longer need to be created by a third party like a bank. All network participants will ensure that each of their ledgers are accurate because an accurate ledger would be in everyone’s best interest. Each participant will hold all the other participants in the network accountable in this type of system. A network like this creates more transparency, reduces the odds that errors are made, and produces a more secure environment in which data can be stored and transacted.

Cryptography

Now that we know what a decentralized network is this gives rise to a few questions, doesn’t it? First, if everyone in the network has a copy of the ledger then doesn’t everyone know everyone else’s personal information? If I look at my ledger can’t I tell which account is yours?

This is where encryption comes in. Cryptography is a method of storing and transmitting data in a particular form so that only those for whom it is intended can read and process it. We all use cryptography everyday. Your online bank account is encrypted and you decrypt this information with your password.

All information that will be stored on the shared ledger can be encrypted using a special type of encryption called asymmetric encryption. We will touch on what the means exactly in a separate article. At this point it is just key to remember that only those who have the means to decrypt any particular data record are going to be able to gain access to it.

Of course you would be able to access the particular data sets that were applicable to you. You would have the password to “decrypt” this information. But if you wanted to understand who owned the account listed underneath yours in the ledger you would not have the ability to do so. You would not have the key to unlock that particular data set.

All that’s important for a decentralized network to operate is the knowledge that other accounts exist and there are participants of the ecosystem. So it is through encryption that we can share all necessary information that is needed to allow a decentralized network to operate without allowing that information to be known to all parties.

Consensus On The Blockchain Explained

Now we can move on to understanding how all transactions are being monitored and processed. If there is no central authority to play the role of transaction validator what is stopping invalid transactions from mistakenly being approved?

The blockchain network prevents this from happening by using algorithms that validate transactions mathematically. Instead of one party approving transaction there are multiple parties competing to solve these algorithms. These “approvers” use very powerful computers in order to solve these algorithms as quickly as possible.

Once one of the validators finds the solution it is shared with all the validators in the network. If a majority of the validators agree with the solution, meaning there is consensus, then the transaction is approved and all the ledgers are updated.

Since blockchain technology uses decentralized ledgers each participant verifies or disputes a particular transaction in a way to keep everyone accountable. In this way we can prevent a particular party from manipulating the ledger or spending more money than they are entitled to.

For example, Joe owns one Bitcoin. Joe wants to buy a used car with his Bitcoin and sends it from his account to the seller. However, Joe is a shady character. Before the transaction for the used car can be confirmed, Joe tries to buy a second car with the same Bitcoin. Joe is trying to spend two Bitcoins even though he only owns one.

Obviously this is not an issue with physical money because you can not spend the same dollar twice. But Bitcoin and other virtual currencies are pieces of computerized information and not physical assets.

Thankfully, the developers of blockchain technology have thought this issue through. We can use a blockchain explained above to prevent the double-spending problem seen with virtual currencies. Although Joe has authorized transactions for two Bitcoins, only the first to be confirmed through the approval algorithm will be processed. Once the first transaction is confirmed all ledgers will be updated and Joe’s new Bitcoin balance will be zero. He cannot send anyone else Bitcoin. All subsequent transactions will be deemed invalid if the sender’s account balance does not match the amount the account holder is trying to spend.

What if Joe tries to dispute this? What if Joe manipulates the code to alter his copy of the ledger to show him having owned two Bitcoin when he really only owned one?

Since everyone on the blockchain network has a copy of the ledger Joe would need to change everyone’s ledger to successfully dispute his balance. His ability to do this is very limited. He probably is only able to update his own ledger and the remaining ledgers he will be unable to alter. The other ledgers in the network would successfully prove that his ledger is incorrect. Think of it as a majority vote. If a majority of the ledgers agree on a particular data point we can assume that the information represented by the majority is correct.

The Power of Blockchain Technology

Through decentralized ledgers, cryptography and consensus an amount of transparency and trust is achieved over and above that which the traditional banking system can offer. This is the true power of blockchain – explained simply, we can use this technology to eliminate the need for a central entity that acts as a sole possessor of account and transactional information.

Blockchain networks already have practical uses in many industries. This technology is already being used today to improve processes essential to the everyday business of financial and healthcare related organizations. Any business that relies on secure and organized data can benefit from using this type of network. This technology has practical use in the world of today and will be a powerful tool in the world of tomorrow.